11 months ago

72

11 months ago

72 ARTICLE AD

Bankrupt cryptocurrency exchange FTX is liquidating assets to repay customers, abandoning plans for a restart due to financial and legal difficulties.

This decision was announced by FTX’s attorney, Andy Dietderich, during a bankruptcy court hearing in Delaware.

FTX filed for bankruptcy in November 2022 and has been embroiled in several controversies and legal challenges. Its founder, Sam Bankman-Fried, has faced fraud charges linked to his company management. According to Dietderich, efforts to find investors or buyers for FTX were unsuccessful, highlighting the company’s lack of sustainable technology and administration. Dietderich labeled FTX as an “irresponsible sham” created by Bankman-Fried.

Despite these setbacks, FTX has reportedly recovered over $7 billion in assets to repay customers. The repayment plan has been agreed upon with various government regulators, who will wait until customers are fully compensated before seeking approximately $9 billion in claims against the company.

A notable point of contention has been the valuation of these repayments. FTX plans to use cryptocurrency prices from November 2022 for calculating repayments when the exchange failed and the market was notably low. The decision has caused dissatisfaction among some customers, as the value of cryptocurrencies like Bitcoin (BTC) has significantly increased.

However, U.S. Bankruptcy Judge John Dorsey upheld this approach, citing the stipulations of U.S. bankruptcy law, which requires debts to be valued at the time of the company’s bankruptcy filing. Judge Dorsey emphasized the lack of flexibility in this legal matter, underscoring the need to adhere to the specific language of the Bankruptcy Code.

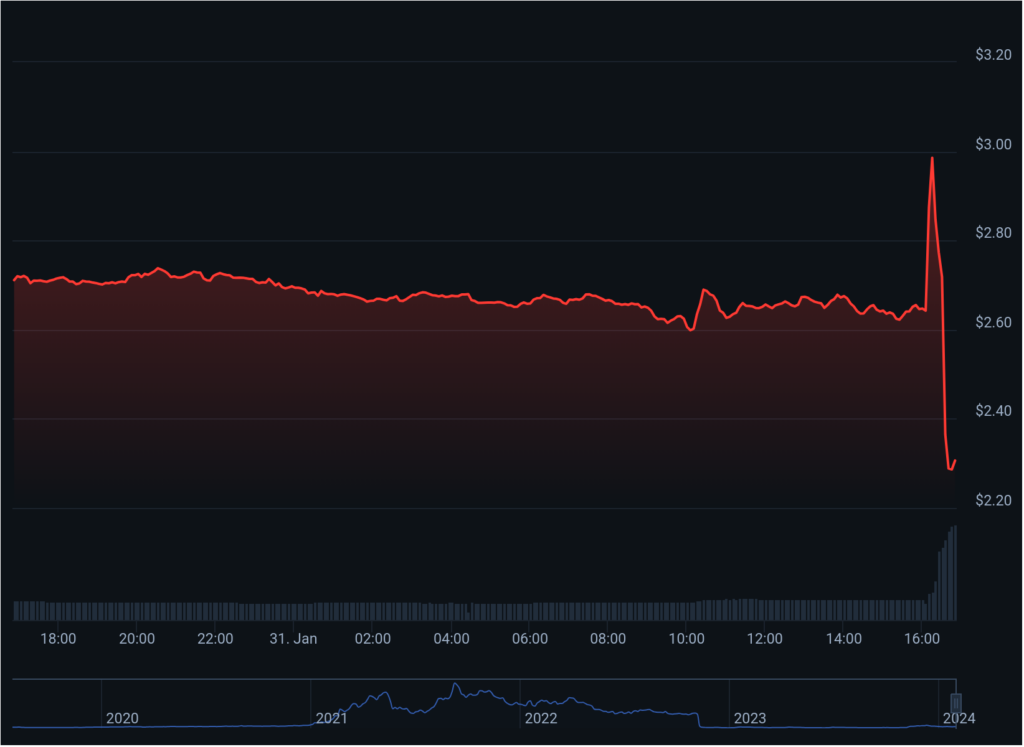

Following this announcement, FTX’s native token, FTT, experienced an over 11% increase in value before dropping 28% down to $2.30, according to CoinGecko.